Risk is a two-edged sword

Take a look at the small print on any investment company’s website: “Past performance is not a reliable indicator of future returns”. That single statement should be a beacon of guidance for all your investing decisions. You can’t bank past performance. Every investment, then, is speculation on the future course of events.

“Prediction is very difficult, especially if it’s about the future.”

Niels Bohr. Nobel Prize for Physics, 1922

The trouble is, as our physicist friend points out, the future is hard to predict. The ability to analyse past events is all that the pros have as their main risk measurement tool. This post will explain how they do it.

Every year, each asset class will rise or fall by a certain amount; whether it be up or down there’s a known movement in the value of all investments. If you were to collect many years’ worth of data you’d be able to calculate the long-term average return for each asset class. Table 2.1, below, shows the returns for the four main Australian asset classes since 2000. Professional investors look at the long-term average return as their best estimate of the expected return from each asset class. It’s almost counterintuitive that the best estimate of the future is the past, especially when money managers remind you explicitly not to draw that conclusion yourself.

| Worst | Average | Best | |

| Cash | 1.7% | 4.5% | 7.6% |

| Bonds | 1.7% | 6.1% | 14.9% |

| Listed Property | -54.0% | 7.4% | 34.0% |

| Shares | -40.4% | 8.2% | 39.6% |

TABLE 2.1: AUSTRALIAN ASSET CLASS RETURNS 2000-2017

One thing you should notice from these statistics is how the return and the risk of each asset class are related. In a previous post we discussed how cash is the least risky and shares are the most risky of our four asset classes. You can see that the average returns of each asset class rise with their relative risk. But the most striking feature of these statistics is how the Best and Worst returns — or, more precisely, how widely these Best and Worst returns are spread from the Average — also rise with the relative risk of each asset class.

This is the two-edged sword of risk: while the average return should increase with the risk of an investment so does the dispersion of the Best and Worst returns from that average. To a professional investor, risk is measured using the average return and a measure of how widely the best and worst returns are dispersed from that average. To a professional investor, risk is a measure of the likelihood that the long-term average — the expected return — will be achieved in the future, whether that be above it or below it.

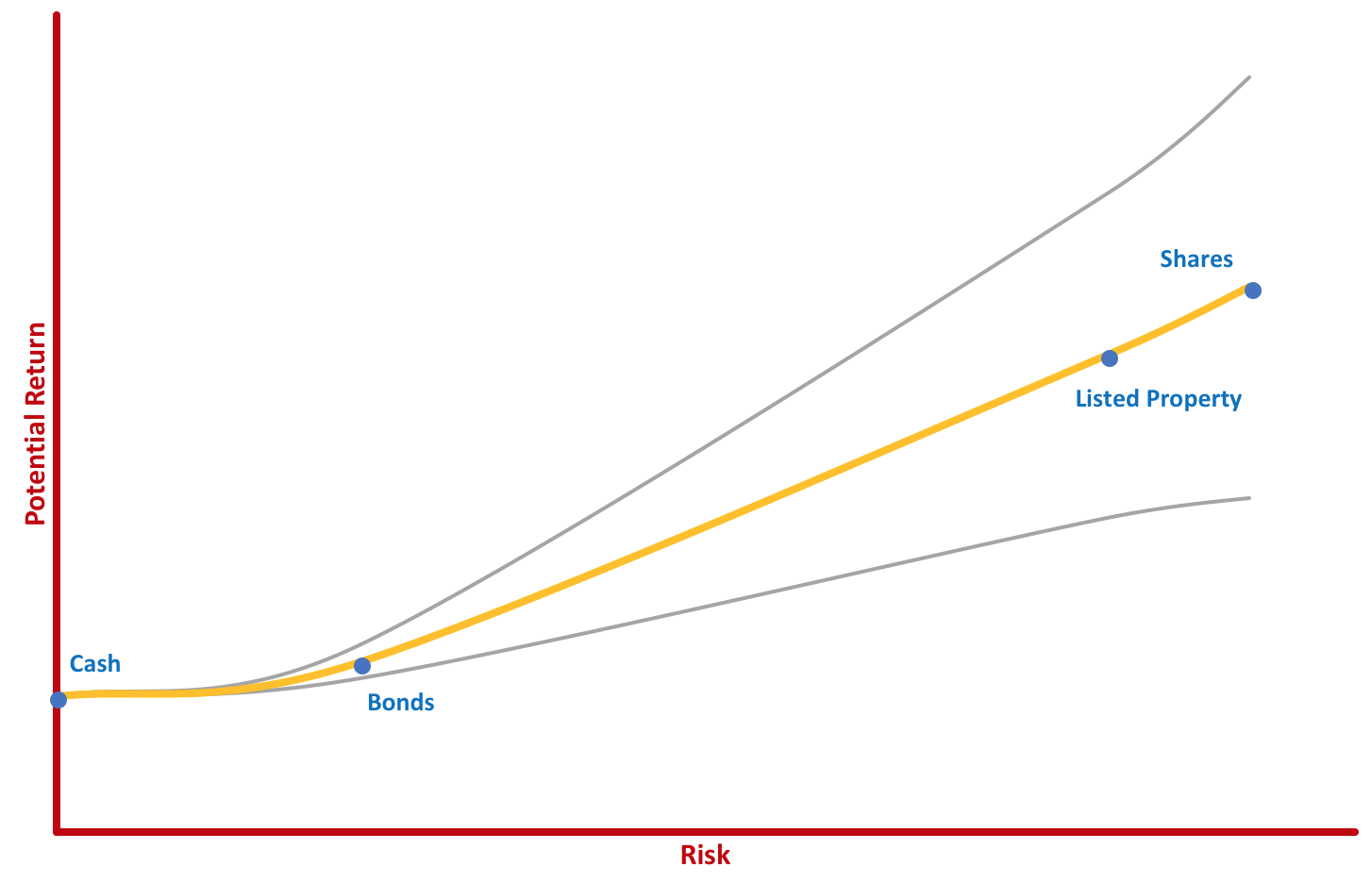

FIGURE 2.1: RISK IS A MEASURE OF RETURN DISPERSION

A shown in Figure 2.1, above, as risk increases the range of possible returns increases. For an investor this means that the higher the expected return the greater the chance that the actual return will deviate from that expectation. In extreme cases, as shown in Table 2.1 the actual return may be negative: the investor will lose money. There are plenty of statistically-advanced ways of calculating these deviations and of analysing the results to produce inputs into even more complex portfolio construction tools but the basic principle remains the same: the risk of an investment — a single investment or an entire portfolio — is a measure of the likelihood that the expected return will not be achieved. The pros call it standard deviation and the higher the number the greater the risk. You could say that it’s a way of measuring the distance between the grey lines in Figure 2.1.

You may wonder why getting a better return than you expected is considered a risk. That’s fair enough since the common conception of risk is that it refers to the possibility of losing money. For all investors, professional and amateur alike, risk should be understood as the magnitude of the possible deviation from expectations: risk cuts both ways. It’s just that it hurts more when it cuts to the downside.

Why it hurts more is a topic for another post.

I’m not quantitatively gifted enough to do this but if only there was a way to methodically apply a points system to deviation of returns such that outperforming expectations did not carry the same weight as underperforming.

Do you think that would help to isolate the dreaded downside risk (risk of loss) or it would artificially lower standard deviations and deceive the consumer?

LikeLike