You’ve probably heard the expression “Time is money”.

Nothing could be more accurate when it comes to the compounding effect of interest. Calculations involving interest start out very easy but rapidly become more complicated. In this post we hope to work our way through some interest rate concepts and show how compound interest can be your best friend.

Get rich doing nothing

If you invest $100 at 5% annual interest with a bank for one year you end up with $105. The interest amount is $5. In this case the interest was calculated and paid once, at the end of the year. This is known as simple interest.

If you were to leave that $105 in the bank at the same 5% for another year you’d end up with $110.25. You earned the $5 interest in year one then you earned interest on $105 in year two. You received 25 cents extra as “interest on your interest”. If you’d withdrawn your interest payment of $5 at the end of year one you’d have missed out on the extra 25 cents.

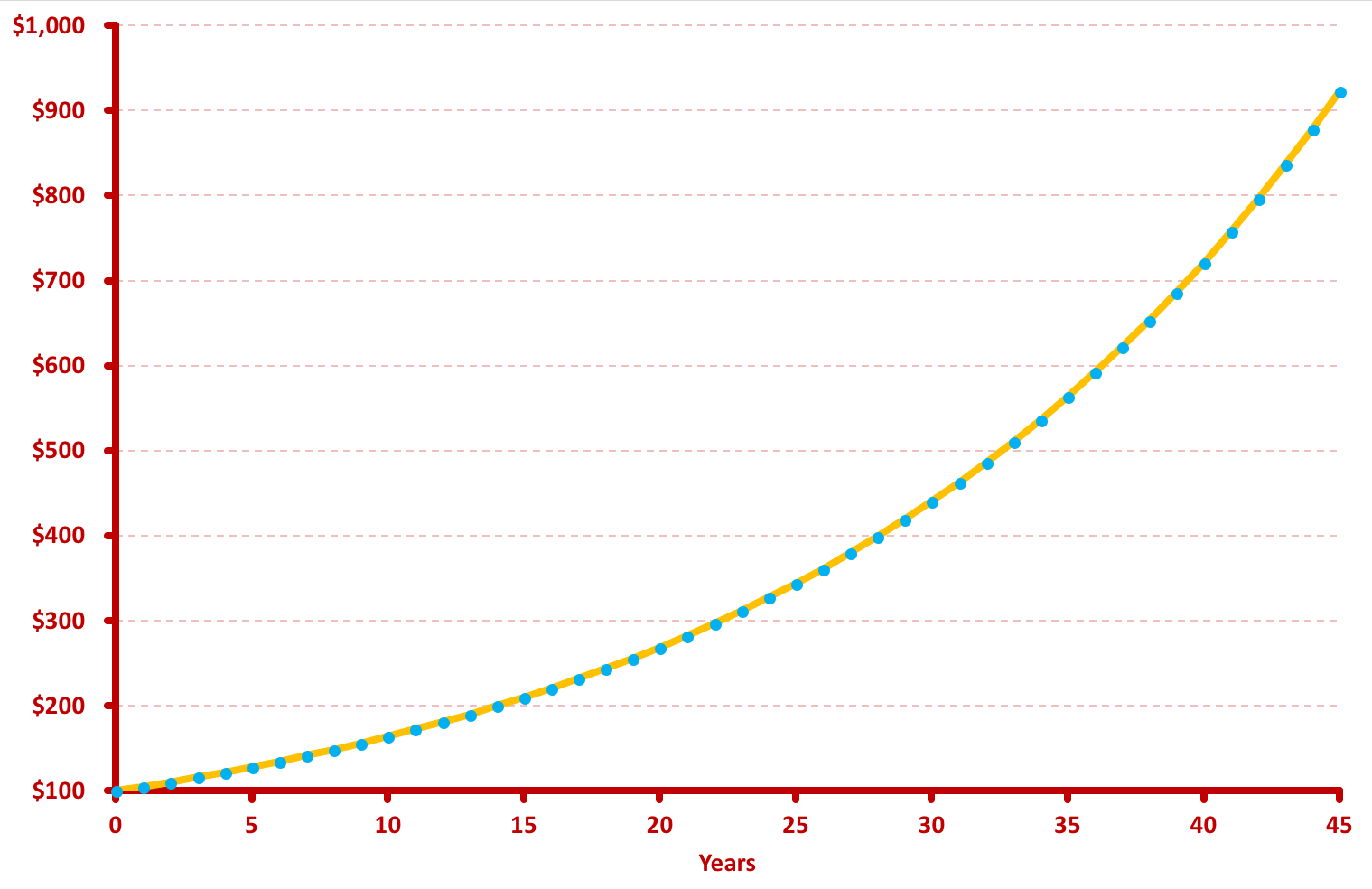

While this doesn’t sound like a lot of money things get pretty exciting after a few more years have passed and this can make a huge difference to the final outcome. Take a look at Chart 3.1, below.

CHART 3.1: COMPOUND INTEREST AT 5% ANNUALLY

CHART 3.1: COMPOUND INTEREST AT 5% ANNUALLY

The longer compound interest works for you the greater the final amount. You’ll notice that the compound interest line isn’t straight. It has an upwards curve in it which shows how compounding speeds up the rate at which your investment grows each year, and it really gets a head of steam the longer it’s allowed to run. In this example, using a 5% annual interest rate, the value doubles roughly every 14 years. After the first fourteen years you’ve earned $100 on your initial $100 deposit but in the next 14 years you’ve earned $200; in the next 14 years you’ve earned $400. So for making one initial deposit then doing nothing at all for 45 years you will have over nine times your original investment (to be accurate, that’s before the tax man takes his cut). There’s the power of compound interest.

Compound interest gets a little more complex to calculate if, as applies to credit cards and mortgages, the interest is calculated more often than once a year. The maths is slightly too advanced for now but, put simply, the more times a year that the compounding is done and the higher the interest rate used, the bigger the compounding effect.

It’s never too early to start saving

I chose 45 years as the time period in our example for two reasons: one is that it clearly demonstrates the power of compounding, the other is that 45 years is close to an average working life. When compounding is put into the context of saving for retirement while you work it can give a very clear picture of the effect that the two parts of compounding — money and time — can produce.

Let’s look at a theoretical example of two people and how they might save over their working life.

Alison starts a job fresh out of university at age 25 and immediately begins saving $2,500 a year; a mere $48 per week. She keeps saving $2,500 every year and is able to earn 5% compound interest until her retirement at age 65. Alison enters retirement with a balance of $317,100 and has only had to contribute a total of $100,000 over the 40 years of her working life.

Alex is Alison’s friend from their university days. He realises at age 40 that saving for retirement is a good idea and also starts putting away $2,500 a year. Alex also maintains his savings of $2,500 per year and is able to earn 5% compound interest until he retires at age 65. Alex’s total contribution is $62,500 over the 25 years but he begins retirement with only $125,284.

Alex has doubled his money but, due to her early start, Alison has tripled hers and is nearly $200,000 ahead. Alex, to achieve the same final balance as Alison, would have had to contribute $6,328 per year or 2.5 times Alison’s annual amount.

When you’re 25 years old the prospect of saving for 40 years seems like forever. Ask someone who’s 65 and they’ll tell you that the last 40 years has flown by in a flash and, given their time again, would have jumped at the chance to save $50 a week. With compound interest time really is your friend.

One final illustration will show the real power of compound interest and the effect of time on your final balance. Table 3.1, below, shows how much you’d need to save each year to reach a $1 million balance by age 65, and the total amount you’d have to put away, depending on your age now. Assuming an interest rate of 5% compounding annually the numbers in the table show that the longer you have to save the less you have to put away to achieve your goal.

| Your Age Now | Annual Amount Invested | Total Invested |

| 20 | $5,660 | $254,712 |

| 25 | $7,469 | $298,776 |

| 30 | $9,965 | $348,771 |

| 35 | $13,498 | $404,953 |

| 40 | $18,692 | $467,291 |

| 45 | $26,758 | $535,152 |

| 50 | $40,426 | $606,393 |

TABLE 3.1: SAVING FOR A $1 MILLION BALANCE AT 5% ANNUAL INTEREST

Take some time now to stop and think what your retirement could look like if you had a cool $1 million when you stopped working. If that money could earn 5% interest you could have an income of $50,000 annually without ever touching the $1 million. Look at your current superannuation balance and compare it to the table above. It may be time to revise your retirement savings plan.

One final word regarding these examples: it’s assumed that the 5% interest rate is earned every year and they don’t take into account any taxes that may have to be paid along the way. Nevertheless, the illustrations tell a compelling story of the need to start saving at the earliest possible opportunity to let the power of compound interest work for you.

With compound interest time really is money; money that’s yours for almost no effort.