Nothing ventured, nothing gained.

Most people are familiar with the general concept of risk and reward: if you’re willing to accept risk you’re likely to be rewarded with something extra at some time in the future. In the financial markets the concept of risk runs a little deeper than the popular conception of the word — which, for most people, signifies the risk of a loss — but the widely accepted rules of the game apply such that the more risk you’re willing to take the bigger your potential reward will be. Note that I’ve used the work potential. This is deliberate because, as we’ll see, almost nothing is certain in the investment world. This is a good starting definition of the concept of risk.

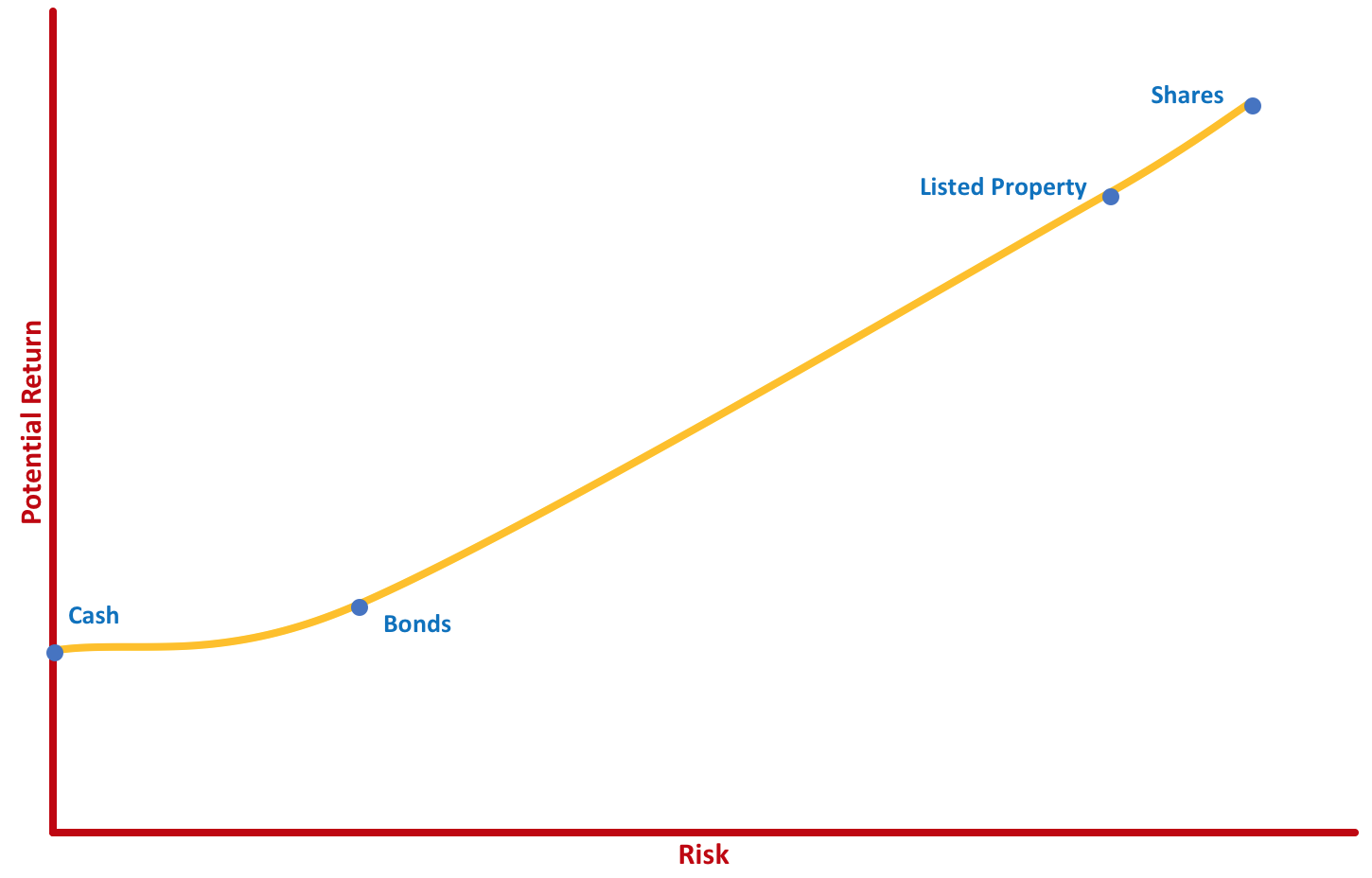

Figure 1.1 below shows the risk/return relationship of some common investment classes. There’s no scale shown on this chart because the actual numbers can change over time; its purpose is to show the relativities between various investments.

FIGURE 1.1: THE RISK/RETURN RELATIONSHIP

Something else to note is that the risk increases with the time horizon of the investment. So an investment in cash, which is a very short-term investment carries almost no risk, and a share investment with a timeframe of seven to more than ten years carries a high risk. In keeping with these risk levels the potential return on each investment is different, with shares having a much higher potential return than cash.

Let’s now turn to the various investment types shown in Figure 1.1 and look at the detail of each of these investments. These are referred to in the industry as asset classes; they represent the major investment categories available to most investors.

Cash

The lowest-risk asset classes are cash and a related short-term investment, bank bills. These are very short-term investments, usually with or backed by banks. Put very simply, with these investments you give your money to a bank and they repay it later with interest. The likelihood of you getting your money back when the investment matures is very high. This is a measure of the credit quality of the banks. Australian banks have what’s regarded as an implicit government guarantee (at least up to a certain amount) which contributes to the very low risk level of these types of investments. Consequently the return potential is relatively low.

The main risk in cash and bank bills is the potential that you won’t get your principal and interest returned when the investment matures. Since the investment timeframe is relatively short (between 1 day and 180 days) the likelihood of a loss is small.

Government Bonds

Next along the risk scale come government bonds. Depending on the credit quality of the government involved (you may know that the Australian federal government has the top credit rating awarded) the return and risk can vary. Investing in Australian government bonds is generally considered a low-risk investment due to its high credit rating.

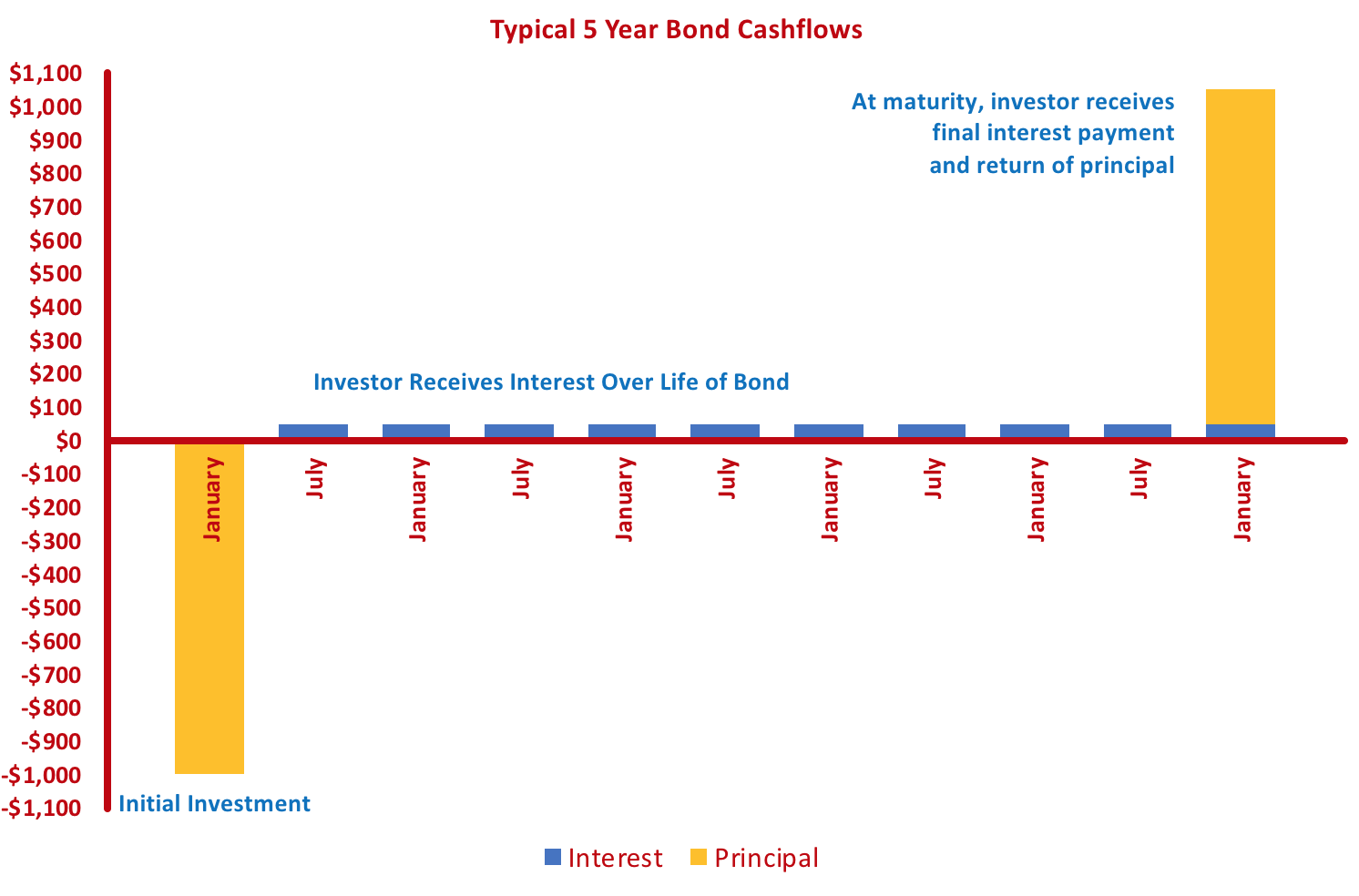

Bonds are typically a long-term investment. A bond is a method for the government to borrow money for a certain length of time — to fund its budget expenditures — with a promise to pay interest twice a year and to repay the amount borrowed when the bond matures. The interest rate to be paid is decided when the bond is issued and remains the same until maturity; this is why these are sometimes called fixed interest or fixed income investments.

FIGURE 1.2: BOND CASHFLOWS

You can see from Figure 1.2, which shows the cashflows of a five-year, 5.2% coupon bond, that after the initial investment, the bond’s cashflows are made up of regular interest payments (often referred to as coupons) until the final interest payment is made along with the return of the initial principal amount invested. This, to be clear, is the happy path of events but it’s certainly not a guaranteed outcome. One of the risks of bond investments is what is called default risk. Default occurs when the issuer of the bond fails to make a payment of either interest or principal when it is due. Investments in high-quality bonds, such as those issued by well-rated governments have a low risk of default. Bonds issued by governments with higher default risk will carry a higher interest rate as compensation for taking on higher risk.

Bonds carry risks in addition to the risk of default, which are not related to the ability of the issuer to make payments when they fall due however they don’t alter the relative risk of bonds compared to other asset classes. These risks will be discussed in a later post.

Listed Property

Australians are said to have a love affair with residential property. For anyone who owns their home it’s probably the most valuable asset in their portfolio (though many may consider their home to be separate to their other investments). But there are other forms of property out there: city buildings, commercial warehouses, shopping malls, car parks as well as large-scale residential developments are all considered property investments. Due to their large scale these investments are potentially out of reach of most investors so the Real Estate Investment Trust (REIT) was devised, initially in 1960 in the United States. The structure came to Australia in 1971 and now the A-REIT market is the world’s second-largest.

The biggest benefit of the REIT structure is that it gives a small investor access to what was previously only available to those with a lot of money. Additionally REITs are listed on the stockmarket so they are easily traded. REITs fall between bonds and other sharemarket investments on our risk chart in Figure 1.1 because they have characteristics of both bonds and regular shares. The REIT structure is required to pay all profits to unitholders each financial year so, on that basis, they are like bonds in that they provide regular income distributions. They are like shares because they’re listed on the stock exchange and are subject to the price movements of other sharemarket investments.

For REITs there are two main risks. The first is that your investment can drop in value if the value of the property that makes up the trust falls; the second is that the value of the dividend falls if the properties in the trust fail to make sufficient profits.

Shares

News of the sharemarket is almost unavoidable these days. Turn on the TV or radio and you’ll hear news of the global market movements almost every hour. It’s the market people hear about the most.

Shares are a risky investment. Depending, of course, on the company you invest in the value of shares can rise and fall, sometimes substantially. Some sectors of the sharemarket are more risky than others. Drug companies can see their shares soar if they discover a cure for cancer. Alternatively their drug trials may fail and their shares become worthless. The mining sector can be affected in the same way.

A company’s ability to pay dividends and achieve growth targets is the primary driver of its share price. The outlook for the global economy, the domestic economy also affect a company’s value. The point to bear in mind is that share prices can fluctuate widely at times and it’s important to remember that investing in shares is a long-term proposition.

Like REITs, shares carry two main risks: the movement of the share price and the level and frequency of dividends paid.

Make your selection

Choosing investments is a little like choosing a car to drive: do you want slow and steady or fast and furious? What reward do you need for the risk you’re going to accept? For how long do you want to invest your money?

The risk/reward tradeoff is yours to select and there are countless ways to mix the assets that you choose for your portfolio (and we’ll cover these in a later post). Just remember that your potential reward depends entirely on how much risk you’re prepared to take.

To learn more about why the payoff for taking risk is only potential reward (or, to use the right term, expected return) see Q2: How do professionals look at risk?

Great introductory post Angus. Although I have always taken issue with the academic definition of risk as it pertains to cash/ bank bills versus government debt.

If I look at Aussie treasury notes versus bank bills or cash in the bank at any one of the big 4, I would have to assume there is some sort of credit risk spread to the bank (corporate) above the sovereign otherwise the big 4 bank bill issuance would be the equivalent or even safer than the treasury notes.

I do appreciate the implicit government guarantee attached to the banks but if their issuance is safer then I smell arbitrage perhaps?

LikeLike