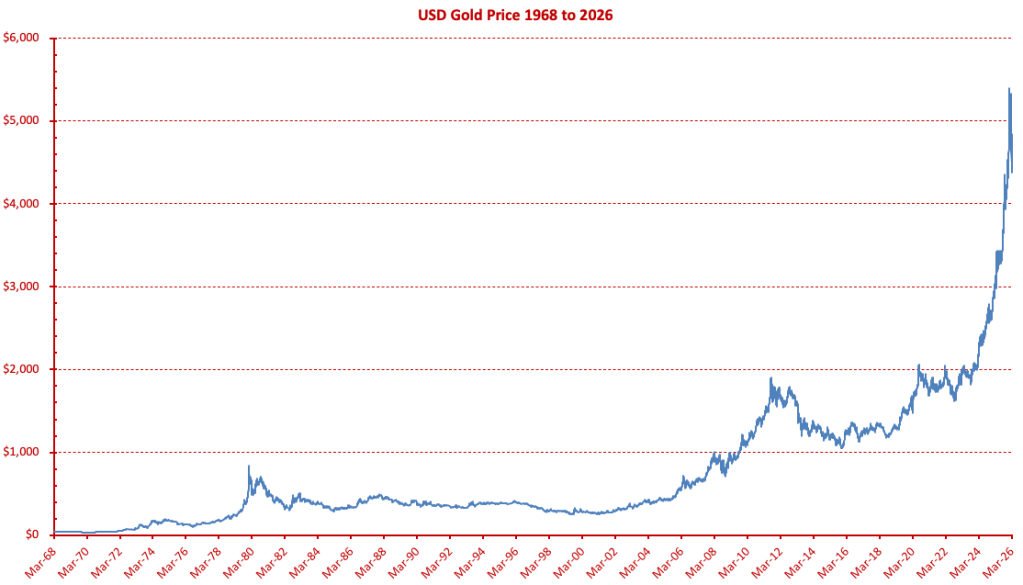

Gold has fascinated humanity for millennia. It is a scientific curiosity, a cultural symbol and a financial asset. While modern investors often think of gold as an investment, its story begins far beyond Earth and its role in portfolios today is shaped by forces both ancient and contemporary.

Cosmic origins and scarcity

The origins of gold are as dramatic as they are distant. Gold is not formed on Earth. It is created in the extreme environments of exploding stars, particularly supernovae and neutron star collisions. These cosmic events generate the immense energy required to forge heavy elements like gold. Over billions of years, fragments of this material became part of the dust cloud that formed our solar system.

The gold we mine today is quite literally stardust. Its extraterrestrial origin helps explain its scarcity. There is only a finite amount embedded in the Earth’s crust and much of it is difficult and costly to extract. This natural rarity has been a key driver of its value across history.

Gold as ornament and symbol

Gold’s scarcity is only part of the story. Its physical properties also made it one of the first metals used by humans. It does not corrode or tarnish, it is easily malleable and it has a distinctive lustre that has captivated civilizations across time.

From ancient Egyptian burial masks to modern jewellery, gold has been used as an ornament and a symbol of wealth, power and permanence. Even today, a significant proportion of gold demand comes from jewellery, particularly in countries like India and China where it plays an important cultural and ceremonial role.

Gold as a financial asset

Gold’s role extends far beyond adornment. It has long functioned as a store of value and a medium of exchange. For much of history, monetary systems were either directly based on gold or linked to it. Although the global economy now relies on fiat currencies, gold retains a unique status. It is an asset that is no one else’s liability and cannot be printed or debased by governments.

This characteristic underpins gold’s importance as an investment. Investors are typically drawn to gold for its perceived ability to preserve wealth, particularly during periods of economic stress. Unlike equities or bonds, gold does not depend on the profitability of a company or the creditworthiness of a borrower. Its value is instead driven by broader macroeconomic and geopolitical factors.

Global instability and safe haven demand

One of the most significant drivers of gold prices is global instability. During times of geopolitical tension such as wars, trade conflicts or political crises, investors often seek safe haven assets. Gold has historically played this role.

When uncertainty rises, demand for gold tends to increase, pushing prices higher. This reflects a basic behavioural pattern. In uncertain times, investors prefer assets with intrinsic value and long standing acceptance rather than assets tied to future cash flows or economic growth.

Inflation and real interest rates

Inflation is another key factor influencing gold prices. Because gold cannot be easily increased in supply, it is often viewed as a hedge against inflation. When the purchasing power of fiat currencies declines, gold may retain its real value.

However, the relationship is not always straightforward. Gold tends to respond more strongly to changes in real interest rates, that is nominal interest rates adjusted for inflation. When real rates are low or negative, the opportunity cost of holding gold decreases, making it more attractive relative to income generating assets.

Central banks and currency movements

Central bank behaviour plays an important role in gold markets. In recent years, central banks, particularly in emerging markets, have increased their gold reserves as a way to diversify away from reliance on the US dollar. This structural demand can support gold prices over the long term.

Currency movements also matter. Since gold is typically priced in US dollars, a weaker dollar often corresponds with higher gold prices and a stronger dollar with lower prices. This adds another layer of complexity to gold price dynamics.

Supply, demand and market flows

Supply and demand dynamics influence gold prices, although supply tends to be relatively inelastic. Gold mining is capital intensive and slow to respond to price changes. New discoveries are rare and production adjustments take time.

On the demand side, investment flows such as purchases of gold backed ETFs can significantly affect short term price movements. Jewellery demand and industrial uses, for example in electronics, also contribute but investment demand is often the dominant driver during periods of market stress.

Risks of investing in gold

Despite its appeal, gold is not without risks. One of the most commonly cited drawbacks is that it does not generate income. Unlike shares which may pay dividends or bonds which pay interest, gold provides no cash flow. Its return depends entirely on price appreciation.

Gold prices can also be volatile. While it is often perceived as a safe asset, its price can fluctuate significantly in the short term due to changes in investor sentiment, interest rates and currency movements. During periods of rising real interest rates, gold prices may decline as investors shift toward assets that offer higher yields.

There are also practical considerations. Physical gold involves storage and insurance costs, while gold backed financial products introduce counterparty and management risks. Investors must consider how they gain exposure, whether through bullion, ETFs or mining stocks, each with distinct characteristics.

Gold as a portfolio diversifier

Given these factors, gold is rarely viewed as a standalone investment. Instead, it is typically used as part of a diversified portfolio. One of its most valuable attributes is its low or sometimes negative correlation with other asset classes, particularly equities.

During periods when stock markets decline, gold may perform well, helping to offset losses elsewhere in the portfolio. This diversification benefit is especially relevant in environments characterised by uncertainty or regime shifts such as changes in monetary policy or geopolitical realignment.

Gold can also serve as a hedge against extreme scenarios. While such events may be rare, they can have significant financial consequences. Gold’s role as a store of value that is independent of the financial system makes it a form of insurance against tail risks such as currency crises or systemic instability.

Ultimately, the case for gold is not about outperforming other assets in all conditions. It is about resilience. Gold’s combination of scarcity, historical significance and independence from traditional financial structures gives it a distinct role in investment portfolios. While it comes with limitations, particularly its lack of income, it can provide valuable diversification and protection in uncertain times.

For investors, the question is not whether gold is a perfect asset. It is whether it has a place alongside others. In a world of complex risks and interconnected markets, even a modest allocation to gold can serve as a stabilising force and help portfolios weather the unexpected.