Robo advisers can offer a cost-effective investment strategy for a fraction of the cost of a human adviser, but they’re not for everyone.

At one time the rise of the machines was thought to culminate in Skynet becoming self-aware and triggering a global nuclear war. Thankfully this has yet to come to pass. We now use computers for more benign pursuits and their application to investing is both helpful and cost-effective.

Many first-time investors begin their journey wondering how to get started. Resources such as TMQ and other on-line and printed financial information give varying degrees of assistance. Many novices end up more confused than when they began. Financial advice can seem like a good idea but, since the Royal Commission into misconduct in the industry, this can be seen by some as prohibitively expensive. Many first time investors don’t have a large amount of money to invest, nor do they have especially complex financial circumstances, so full-scale financial advice is not appropriate for them.

So what options do small balance, first time investors have? If going it alone seems too daunting a robo adviser may be a prudent way into the world of investing.

Give some info, get some answers

If full-scale financial advice isn’t your thing a robo-adviser may be for you. Not a Terminator-style robot giving you financial tips, robo advice is financial advice that caters for broad categories of investors and creates cheap and easily purchased diversified portfolios of investments.

We’ve written previously about diversification as a valuable way to limit the risks involved in investing. By creating portfolios of various asset classes — such as bonds, domestic and international shares, precious metals and other assets — an investor can benefit from their uncorrelated price movements. We’ve also written about ETFs which allow investors to invest in broad ranges of assets within each investment category.

Robo advisers bring diversification and ETFs together to create portfolios of assets for investors.

Portfolios made for people like you

You’re probably wondering what the robots at robo advisers do for you. After asking a few questions about your objectives, your risk tolerance and your time horizon, robo advisers then suggest a portfolio of assets that would be generally suitable for investors who share investment goals. It’s not specific, personalised advice like you’d get in a full-scale financial plan but it’s a generally pertinent portfolio for your needs as assessed by the answers you’ve given to the short questionnaire.

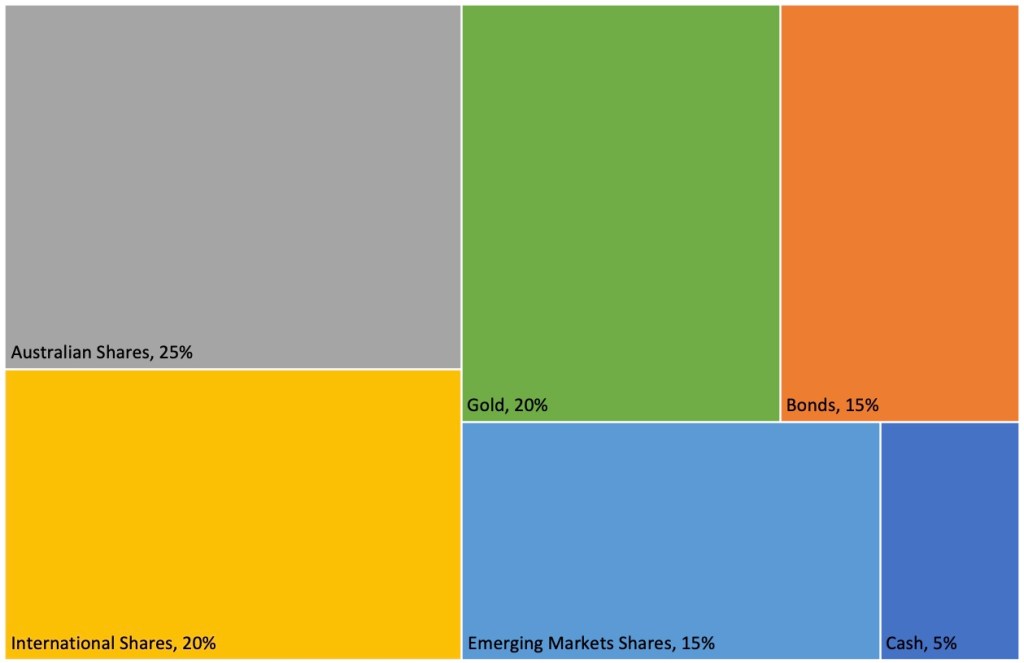

Robo advisers recommend a portfolio of assets for your savings. These are made up of separate asset class components which are often ETFs. A robo adviser’s suggested portfolio might be made up of a set of ETFs such as the example below (this one has a lot of share market exposure and some gold):

There are six components to this portfolio and each would be obtained by an investment into an ETF selected by the robo adviser in the porportions indicated. Various blends of assets would be available to allow for different risk and return combinations from very conservative, with more defensive assets such as bonds and cash, through to very aggressive, with more domestic and international sharemarket exposures. Each ETF unit is purchased by the adviser and held under your own name using the stock exchange registry system; you actually own the assets yourself.

Getting the balance right

The portfolios’ allocations to each asset class will move away from the initial proportions as the prices of each ETF change. When you add more money to your account the adviser will direct your cash so the balance is maintained as you increase your investment. Some advisers will allow you the option to have your account automatically rebalanced once or twice a year if you’re not making regular investments. Either way, your portfolio stays on track to deliver the return and risk outcomes that were selected when you began.

Information at your fingertips

Robo advisers usually have a useful website, and even a smartphone app for you to check your investments and to add to, withdraw from or change your investments. You can see your investment performance and other relevant information for tax and financial planning needs, too.

What’s this going to cost?

Robo advice includes the fee that’s built into the ETF plus a charge for the robo adviser’s services. This will typically be around 0.50% of your assets and certainly less expensive than full advice. TMQ always suggests shopping around to find the robo adviser which gives you the best value for your fees.

I’ll be back

Those with special needs or complex tax positions will probably not be the target clients for robo advice. Take some time to survey the robo adviser landscape and to find one that’s right for your situation and needs. For a typical uncomplicated investment portfolio you may find that robo is the right type of financial advice for you.