Little by little you could be literally giving away your nest egg

For most Australians their superannuation fund is the biggest investment they’ll ever make aside from their home. The design of the super system is that, over nearly a half-century of your working life, you accumulate enough money to be able to live comfortably in your retirement years. You put away about 9.5% of your salary every year. A good selection of investments, plus compound interest, should leave you with a nice nest egg to begin your retirement years.

It’s fairly simple to understand when it’s worded like that but, of course, the real world adds some complications. It’s these complications which can slowly erode your retirement savings. The purpose of this post is to help you to identify them and to find ways to minimise their effects on your savings.

In May 2018 the Australian Productivity Commission released a draft report about superannuation. I’ve linked it here but at 549 pages it’s quite a long read. The report identified what has been well-known in the industry for some time: the complexities and inefficiencies in the industry leave many people worse off than they should be.

Cost control

According to a report by the Australian think-tank The Grattan Institute, less that half of superannuation fund investors know what the fees are on their account. Perhaps more worrying is that many more may not fully appreciate the effect of fees on their final retirement balance. Understanding how fees eat away at your nest egg is vitally important. In this post we will show you a few examples of why fees are your worst enemy.

Super is unfortunately rife with fees and charges. There are fees to manage your account, additional administration charges, performance fees, establishment fees, contribution fees, switching fees and life insurance premiums all being deducted from your retirement nest egg. For most super accounts the biggest fee is the management fee. Luckily this is a fee over which you do have control: you can choose to switch to a fund with a lower fee.

Here’s why it’s a good idea to shop around for a cheaper fund. Let’s say you are 21 years old and have just started work earning $50,000. Using some reasonable assumptions about pay increases and the returns on the investments the Productivity Commission estimates that for every 0.50% increase in your super fund fee you will have $100,000 less in retirement. So if you lower your fee you raise your final balance.

The Grattan Institute did a similar estimation of the reduction in your final retirement balance as fees increase. As shown below, for every 0.50% increase in fees your super balance reduces by around 10%.

From the lessons you learned in the post on compounding you’ll know that the longer the time period the larger the compounding effect, and the higher the compounding rate the larger the effect. You can use this knowledge when you look at fees. At first glance a fee of 1.5% appears very small. If you were offered a discount of $1.50 on a $100 purchase you probably wouldn’t care much. But if your super fund will be taking 1.5% of your money every year then this means the rate at which your nest egg is compounding is reduced by 1.5% each year. Average returns, pre-fees, are likely to be around 6% to 7%. Take off the fund’s fee and the amount left over for you is much less.

The chart above means if your fund charges 2% in fees you will have paid away over one-third of your own money in management fees. If your fund charges 0.50% then you’ll have only paid 11%. That’s a difference of around a quarter of your money that you’ve effectively given away to a fund manager. The good part of this story is that, with just a small amount of effort on your part — most of it done on the internet while you have a cup of coffee — you could potentially save yourself a lot of money and set yourself up for a much better retirement. Imagine what you could do if you had an extra $100,000 when you retire. European vacation, anyone?

According to the RateCity comparison tables the lowest-cost fund charges around 0.49% annually to manage their members’ super while the highest-cost fund charges 2.99%.

This difference is amazingly large and you may be left wondering why there’s such a huge range of charges. I know I am.

Poor performing funds

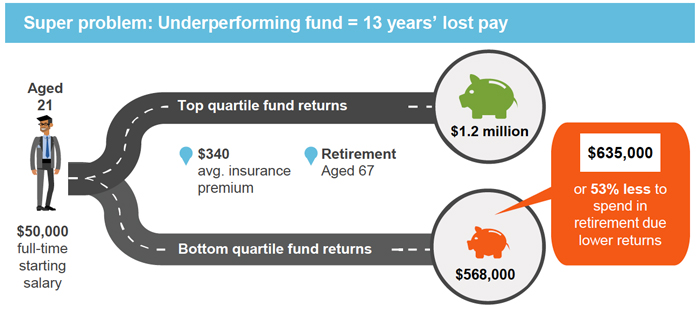

You can’t pick your fund’s investment performance in advance, but the Productivity Commission’s draft report analysed all superannuation funds on offer. The graphic below shows the difference in final retirement balance between investing in a fund with performance in the top 25% of funds and investing in one in the bottom 25%.

[Source: Productivity Commission]

The difference is a massive $635,000, or more than a 50% reduction in the final balance from best to worst. Again we see the effects of compounding on long-term returns and this example shows in sharp detail and hard numbers just what you might be giving up with a poor choice of super fund.

If you’re unlucky enough to be in a high-fee, low-performing fund then you are being skewered twice. Your retirement balance and therefore your retirement lifestyle will be vastly different, and not in a good way.

A call to action

The first thing you can do is to check your super fund’s fee. It’s difficult to see it on your statement as it’s often stated as a dollar amount rather than a percentage charge. Call them. Ask them questions, especially about their fees.

The next step is to check other funds. Look up their performance numbers. Look at longer-term numbers, longer than five years. How does yours compare? If you don’t think you can manage this yourself, seek out the help of a financial adviser.

If you find a better fund than you’ve currently got, and if your employer allows it, make the switch. Often the fund you want to move to will do all the administration for you. All you have to do is complete a form and email it back to them.

You can do this today. You should do this today. Don’t put it off.

One more positive action you can take is to make sure you only have one superannuation account. You may have had a few jobs and it could be that in each one your employer opened a new account for you. All these super funds will be taking their fees and insurance from your money. You can only ever claim on one insurance policy so you’re literally throwing money away paying premiums on more than one account. These insurance premiums average around $340 per year per account.

If you’re young and you think “all this super stuff is way off in the future” then just remember the power of compound interest. Do it now and reap the compound benefits in the future. If you’re not young then do it anyway.

There’s no time like today to make your own future better.